Market Trends

Stephens will never ask clients or prospective clients for personal or financial information, or provide investment advice, via social media, or WhatsApp.

If you have any questions or concerns about someone from Stephens contacting you, please call your Stephens Representative or reach out to us via our Contact Us form.

We provide investment banking, research, sales and trading, asset and wealth management, public finance, insurance, private capital, and family office services.

We are a family-owned financial services firm that values client relationships, long-term stability, and supporting the communities where we live and work.

The idea of family defines our culture, because each of us knows that our reputation is on the line as if our own name was on the door.

Our reputation as a leading independent financial services firm is built on the stability of our longstanding and highly experienced senior executives.

We are committed to bettering the communities where we live and operate. We do this by supporting corporate philanthropy, economic and financial literacy advocacy, and professional success.

Stephens is proud to sponsor the PGA TOUR, LPGA Tour, and PGA TOUR Champions careers, as well as applaud the philanthropic endeavors, of our Brand Ambassadors.

Stephens is the official investment banking partner of Williams Racing, one of the most winning teams in F1 history. We share that tradition of success.

We host many highly informative meetings each year with clients, industry decision makers, and thought leaders across the U.S. and in Europe.

We provide fiduciary investment strategies to public-and private-sector institutional clients through asset allocation, consulting, and retirement services.

Decades of proven performance and experience in providing tailored fixed income trading and underwriting services to major municipal and corporate issuers.

Proven industry-leading research, global market insights, and client-focused execution.

Customized risk management, property & casualty, executive strategies and employee benefits solutions that protect our clients over the long term.

We assist companies with accessing capital through innovative advisory and execution services that help firms achieve their strategic goals.

We have been a trusted and reliable source of capital for private companies for over 70 years.

Our experienced Private Client Group professionals develop customized investment strategies to help clients achieve their financial goals.

We are a trusted municipal advisor with proven expertise in public financings. We also work with clients in negotiated and competitive municipal underwritings.

Market Trends

Over the course of the last several years, M&A activity in the Value-Added Warehousing (“VAW”) sub-sector of the Transportation & Logistics (“T&L”) industry has ramped considerably. In this article, we reflect on some of the key factors that have helped drive this market interest and share perspectives on some important themes for industry participants, now and in the years ahead.

At a high-level, some buyers may view the Value-Added Warehousing space as uniquely positioned to possibly benefit from several potential long-term macroeconomic tailwinds.

The combination of these factors is fueling growth in the VAW subsector of the T&L industry. In the 5 years leading up to Covid-19, the Value-Added Warehousing space grew at a 6% CAGR[5]

Through 2027, the global industry is forecast to grow at an 8% CAGR[6]. Given the potential organic growth, market interest levels could grow in the years ahead.

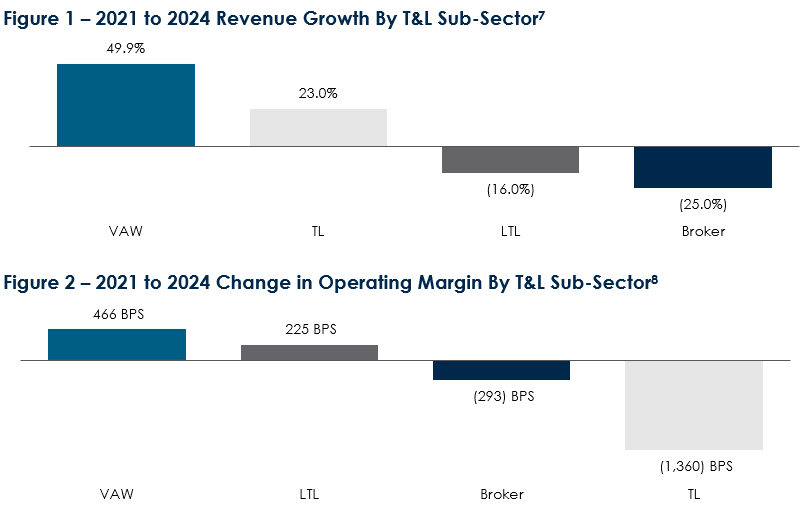

Most VAW services are contracted with clients, oftentimes on a multi-year basis. Contract conventions vary by end-market and service, but in general, tend to provide for high-levels of revenue visibility as compared to other, more transactional types of logistics services, such as trucking, brokerage and freight forwarding. Levels of integration with clients tend to be high, with new project lead-times often being 6 months or more to accommodate for customized service preferences. This dynamic could result in significant switching costs, potentially leading to strong levels of client retention. Over the course of the most recent freight market downturn, Value-Added Warehousing models have exhibited strong levels of growth and margin stability relative to other T&L sub-sectors, as evidenced in Figures 1 and 2 below. This predictability and lack of cyclicality has helped drive strong recent buyer and lender interest.

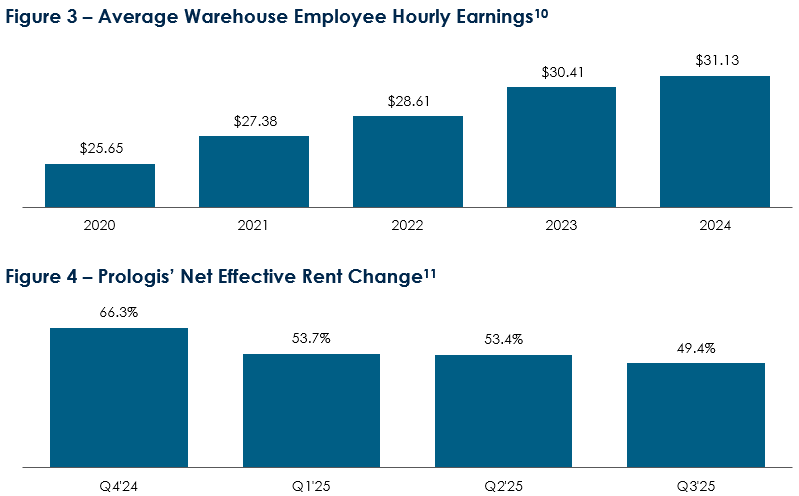

The North American total addressable market for VAW services is in excess of $250 billion[9]. This market is dominated by small, regional participants with few providers commanding a meaningful share of total industry revenue. This fragmentation could create significant competitive opportunities for those with scale. Small regional providers often lack the internal engineering processes to effectively design complex client projects. Smaller players are also less likely to have invested in sophisticated technological systems that allow for more robust analytics and customized reporting that clients are increasingly requiring. Finally, providers with scale are much better positioned to manage through the largest cost categories that present the greatest potential for margin compression: labor and real estate. In Figures 3 and 4, we highlight recent U.S. trends in hourly labor rates for warehouse employees and the average rate of increase at lease maturity for Prologis across its U.S. warehousing property portfolio, respectively.

For providers without a scaled human resources function (or negotiating power with staffing agencies) or relationships with national landlords, cost pressures have been acute in recent times[12].

Sub-scale providers are often the perfect M&A targets for strategics pursuing a consolidation effort in the sector. The valuation discrepancy between a provider with scale (>$10m EBITDA) and a smaller provider (<$5m EBITDA) on an EV / EBITDA multiple basis can be substantial given the difference in risk. When executed effectively, M&A helps strategic acquirers enter new services or geographies, gain exposure to new customers and end markets, and bring on additional talent. Cost synergies for transformative transactions are potentially meaningful, but in bolt-on transactions tend to be more limited. That said, relative to other areas of logistics, integration risks are more limited given individual facility operations are semi-autonomous in nature.

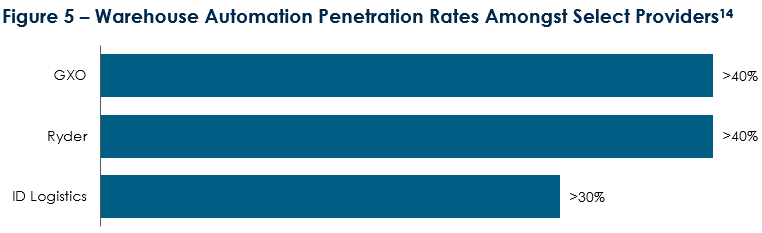

Ongoing innovations in automation tools have helped to dramatically improve labor efficiencies for providers that are able to effectively implement and utilize such technologies. While costly, automation is becoming increasingly common, further deepening the potential competitive moats for those with scale. According to the International Federation of Robotics, the market for industrial robots more than doubled over the course of the last decade to 542,000 installations in 2024, driven by new user adoption[13]. As shown in Figure 5, large public providers are implementing automation technologies in situations where both the economic and use case are viable. In the years ahead, this penetration rate could grow materially as innovation comes to areas of the Value-Added Warehousing market where no solution exists today, such as bulk pallet storage and handling.

Despite this attractive backdrop, there are risks that are unique to the Value-Added Warehousing space that need to be properly reviewed and understood. High levels of customer concentration are common in the sector, so understanding a target’s relationship with its key customers is critical. Mismatches in facility lease terms with key customer contract maturity is another common area of focus in business diligence. Finally, given the duration of contracts are typically multi-year, understanding the mechanisms to offset areas of cost inflation that providers are likely to experience over the life of a client engagement, such as in labor or leases, are important for understanding contract economics.

Over the course of the last ~15 years, Stephens has built a market leading Value-Added Warehousing and contract logistics practice, closing over 10 transactions in the sub-sector.

Stephens Investment Banking: Transportation & Logistics

For more information on Stephens’ capabilities and experience

in the VAW sub-sector, please contact either of the authors below: