Clients,

We have modified the approach to our IB Quarterly Update. While historically we have focused on content relevant to each industry group, we have determined that the macro trends impacting businesses may be more helpful.

We are in a very interesting period for the markets. While there is no shortage of trends that we could discuss, we believe the following are most relevant, and explore each of them in depth:

- Credit - while still accessible; pricing and terms are changing

- The bar for processes is rising and buyer interest is largely dependent on the quality of the company

- Strategic buyers are gaining some advantages

- Deal certainty is taking precedence over top ticking valuation

I hope you find this edition useful.

Sincerely,

Brad Eichler

Executive Vice President, Head of Investment Banking

SELECT QUARTERLY TRANSACTIONS

To see all Stephens Investment Banking transactions & advisory assignments, click here.

EXPECT FURTHER M&A ACCELERATION IN UK-BASED ASSET AND WEALTH MANAGEMENT

Hugh Elwes, Managing Director in Financial Services, explored how, as markets continue to digest the effects of the crisis in Ukraine and the ongoing pandemic recovery, fresh momentum has returned to the M&A space for asset and wealth management companies. Fee pressure continues to intensify – driven by customers seeking better value for money and heightened transparency. The UK may experience continued action from asset managers, as the sharp rise in inflation, as well as ongoing supply chain issues and enduring pandemic-related pressures, still pose risks to many groups. Click here to read more.

FINANCIAL SPONSORS UPDATE: HEALTHCARE SERVICES SPOTLIGHT

Financial sponsors continue to show significant interest in critical outsourced services supporting the U.S. healthcare system. In particular the healthcare linen management space has received considerable attention. Long-term contracts, focus on quality and reliability of service, and insulation from reimbursement risk provide favorable dynamics that have attracted PE investment. As hospitals continue to consolidate, outsourced providers have been following suit in order to support their customers’ larger footprints. Read the brief here.

BUOYANT SUPERRETURN IS EVIDENCE OF PE'S TRANSITION TO MAINSTREAM ASSET CLASS

Simon Tilley, Managing Director in the Financial Sponsors Group, was published in Private Equity News writing about takeaways from the SuperReturn event held June 14-17 in Berlin. The main theme at the last pre-pandemic SuperReturn in February 2020 was the transition of private equity from an alternative to mainstream asset class. Fast forward to the just completed 2022 iteration of the event and this evolution has further accelerated. A host of LPs and GPs were in attendance at the Berlin-based SuperReturn this month, with a supporting cast of thousands of bankers, lenders and industry service providers. One of the key takeaways from the event was the buoyant fundraising backdrop. Click here to read the article.

CREDIT - WHILE STILL ACCESSIBLE, PRICING AND TERMS ARE CHANGING

OVERVIEW

As public credit markets have experienced significant spread widening and more conservative leverage profiles, the private credit markets have remained competitive for quality businesses and for appropriately structured credits. Credit is still available, but private credit market conditions are tightening. The appetite to lend is becoming more binary and selective – for both banks, which remain extremely well capitalized, and private credit. It is no longer sufficient to merely increase the yield on mediocre credits.

Banks Are Less Accommodating

In the current ESG and macroeconomic environment, banks are less accommodating to borrowers facing near-term challenges than they would have been during the previous two years, when pandemic pressures made it infeasible for banks to rigorously pursue workouts or amend financial terms to borrowers. Banks and private credit funds could deem some businesses less attractive in today’s turbulent environment. This is likely to strain relations between lender and borrower. As businesses look to become more nimble in uncertain times, so do lenders. This dynamic will also drive the demand for new credit. This is just one of many factors that could cause rates and terms to be more favorable to lenders in the coming months.

Private Credit Spreads Slightly Elevated

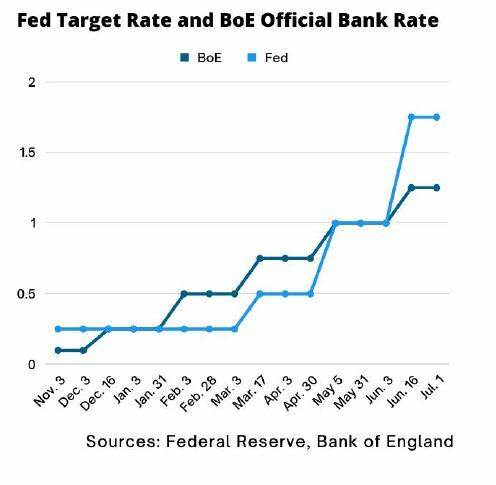

Risk spreads in the private markets are only slightly elevated. Most of the increase is due to movements within the floating SOFR and SONIA benchmark rates as a result of rate hikes implemented to combat inflation by the Federal Reserve[1] and Bank of England[2], and the potential for additional ratehikes by the European Central Bank[3]. In the near term, many private credit investment committees are likely to maintain current rates or enact only slight increases. However, credit committees will have a laser focus on resilience to labor shortages, supply chain issues and other macroeconomic factors. The premium for risk likely will widen over the coming months as these factors begin to materially affect businesses. By Q4, yields may accelerate and it may become more difficult to obtain even private credit.

Liquid vs Illiquid Markets

Another potential catalyst for rising private credit spreads is relative value. Some private credit funds have been able to achieve outsized returns by deploying capital in what are currently very disjointed, liquid credit markets throughout the first part of the year. So long as private credit funds are able to achieve a greater risk/return profile in the liquid credit markets, access to private credit in the illiquid markets will remain constrained and more costly. Therefore businesses that plan on accessing credit markets later this year may benefit from evaluating all options, approaches, and timing sooner rather than later.

PE Seeing Minimal Leverage Compression

Yet, so far, top quality private equity-owned companies in strong sectors have not experienced much leverage compression, and it remains uncertain whether a major shift in leverage is under way in the lower and middle markets for PE transactions. Although, higher pricing probably eventually will impact PE valuations as cyclical sectors, including certain consumer subsectors, see lower leverage.

Sources: Federal Reserve Bank of New York, Bank of England, European Central Bank

THE BAR FOR PROCESSES IS RISING AND BUYER INTEREST IS LARGELY DEPENDENT ON THE QUALITY OF THE COMPANY

OVERVIEW

Anecdotal evidence suggests that, at the end of Q2, the number of initial indications of interest submitted for M&A deals was down by about a third compared with activity 12 months earlier. Buyers are focusing on transactions where they have meaningful points of differentiation, the highest potential for return, and/or those opportunities that buyers are most confident they will win. Interestingly, despite global M&A deal volume falling from Q1 to Q2[4], deal value increased during that time period.

M&A Requiring Distinct Buyer Advantage

Perhaps more than ever, mergers and acquisitions must come with some distinct advantage for a buyer. These include synergies, exceptional management teams, significant historical experience, a differentiated thesis for long-term growth, and a path toward future deals. In the absence of advantages like these, generating sufficient interest may be a challenge. Even with these advantages, many buyers are still questioning if now is the right time to deploy capital. Indeed, some buyers are prioritizing capital preservation, focusing on their core competencies, and bracing for a potential recession.

PE Deciding Quickly on Potential Deals

Financial sponsors have been deciding quickly, either against acquisitions or aggressively pursuing them, with somewhat greater intensity than they had in 2020 and 2021. This makes pre-process buyer education the key to successfully running a narrower process. Private equity firms appear to be especially interested in top-quality services-oriented companies in sectors that have avoided steep supply chain disruptions, labor shortages, and other macroeconomic shocks in the first half of 2022.

A Premium Put on Resilience

To be sure, well-managed companies in sectors that face moderate levels of such headwinds also are garnering PE interest, albeit to lesser extents. And while PE firms specializing in distressed / turnaround companies are eagerly anticipating opportunities, businesses in cyclical sectors may be a tough sell overall. Over the next 12 to 18 months sellers may see a premium for demonstrating resilience, which has become at least as valuable as demonstrating growth.

PE Dry Powder Increasing

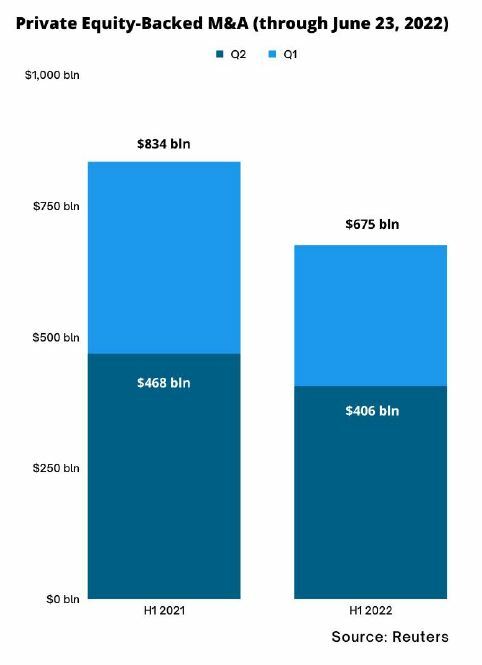

During 1H 2022, the total value of PE-backed M&A deals fell 19%[5] compared with the same period last year, from approximately $834 billion to approximately $675 billion. Meanwhile, equity and debt dry powder is increasing. As of June, total available capital was estimated at approximately $1.86 trillion[6], up from approximately $1.81 trillion at the start of 2022, with the largest 25 PE firms holding approximately 25%[7] of this amount.

Sources: JDSupra, Reuters, MarketsGroup, Allvue Systems

STRATEGIC BUYERS ARE GAINING SOME ADVANTAGES

OVERVIEW

With some public stock prices down 20%-50%, certain strategic acquirers may be in a better position to pursue public company M&A deals that would not have made financial sense at the uncommonly high valuation multiples and stock prices that had prevailed in the past couple of years. Public strategics may be able to use their stock as currency, offering valuable liquidity and future upside to targets.

Strategic M&A Multiples at Record Levels

Globally, the biggest M&A deal announced in Q2 was the planned $61 billion cash-and-stock acquisition of VMware by Broadcom[8]. After dipping to 11x EV/ EBITDA in Q1, multiples on strategic M&A deals returned to record levels at 16.7x in Q2[9].

Ample Cash, Minimal Financing Risk

Well-capitalized strategics that are intent on dealmaking have great potential to conduct successful acquisitions in this environment. This is particularly the case for strategics with cash and access to undrawn credit facilities, which pose minimal financing risk. These companies can act quickly without undergoing a time-consuming debt financing process.

Synergies and Long-term Strategies

They also may benefit from synergies while executing their strategy over the long-term. Whereas some acquirers may accomplish this by augmenting current lines of business or entering complementary ones, the long-term strategy also may involve expanding into new geographies, developing essential technological capabilities, while achieving scale and/or gaining market share.

PE Remains Competitive on Acquisitions

Although these factors are helping strategics to become better positioned with companies facing certain macroeconomic or sector-specific headwinds, private equity firms continue to compete effectively for acquisitions of companies that are performing fairly well – and especially for targets in sectors in which the PE firm has both deep experience and a strong track record. Furthermore, as large global corporations review their portfolio of businesses to distinguish core from non-core activities, PE firms are poised to transact on a range of those non-core disposals.

Sources: Reuters, Bain & Company

DEAL CERTAINTY IS TAKING PRECEDENCE OVER TOP TICKING VALUATION

OVERVIEW

It is still possible that 2022 will turn out to be very strong for M&A, with the potential for total deal value to reach $4.7 trillion – which would be the second-best year on record[10]. Among the host of factors potentially complicating deals in the second half of 2022, buyers and sellers alike have been focusing on inflation, rising interest rates, labor shortages and costs, supply chain disruptions, COVID-19, Russia’s war in Ukraine, upcoming U.S. mid-term elections, and the increasing probability of recession[11].

Preemptive Deals on the Rise

As a result, sellers that once were comfortable with pursuing broader M&A processes along standard timeframes have begun to reevaluate whether they should instead seek to complete deals earlier, at solid valuations with parties that already have shown interest. In the past few months there even has been a material increase in preemptive deals where timing and certainty of closing have taken precedence over achieving the maximum potential pricing opportunity.

PE Sellers Seek Financing Certainty

In M&A transactions, sellers are demonstrating a greater willingness to prioritize deal certainty instead of risking delays amid broader macroeconomic or geopolitical concerns. For PE sellers – which traditionally have been reluctant to accept valuations that fall below their own expectations – financing certainty has risen in importance, especially where significantly fewer buyers have been bidding in processes.

Momentum Deals Give Way to Fundamentals

If a recession does occur, PE firms may find it more challenging to conduct preemptive deals while also performing thorough due diligence in a market that returns to focusing on fundamentals and away from the momentum-based deals of the past few years. The overriding questions are whether valuations will deteriorate further, and if so to what extent. The willingness to pay lofty valuations has decreased, across many sectors, for all but the most sought-after companies.

Increased Use of Continuation Funds

Finally, it is worth noting the increasing use of continuation funds, where PE firms effectively sell the best assets in their portfolios to special purpose vehicles set up by themselves. In addition to a mix of existing and new investors, continuation funds may allow general partners to continue working with proven, successful, portfolio companies during a market downturn with the goal of further growing the business and exiting in the longer term in a better market environment.

CONCLUSION

One of the few certainties in this period of extreme volatility is that challenging times highlight the need for a skilled advisor that is experienced at considering all options. The window for deals is opening and closing at a more rapid pace. Both financial sponsors and strategics must be fully prepared and ready to take advantage of market opportunities as they emerge. In some cases, broad processes may not always be the best solution. Buyers and sellers require an advisor that truly understands the market and how to approach each deal. With deep knowledge across the spectrum of investment banking services and sectors, about how historical trends and the latest developments are shaping opportunities for clients, Stephens is ideally suited to serve as that advisor.

Sources: Associated Press, Federal Reserve Bank of Atlanta, Stephens Inc. Viewpoint Economic and Financial Commentary

About the Expert