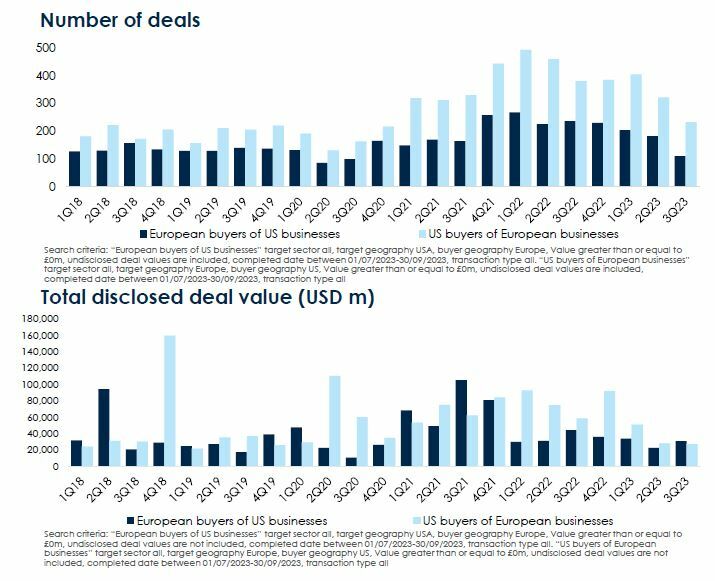

Overview of transatlantic deal activity: 2018 to present

The nine quarters up to the end of Q1 2020 – the onset of the Covid pandemic – averaged 196 US acquisitions in Europe per quarter. The level of quarterly dealmaking activity naturally dropped sharply as Covid hit, but then consistently and dramatically increased on a quarterly basis to a peak of 493 US acquisitions of European companies in Q1 2022. However, the level of US acquisitions in Europe has since fallen back towards pre-pandemic average levels (233 in Q3 2023).

For European acquisitions of US businesses, the nine quarters up to the end of Q1 2020 averaged 135 deals per quarter, again dropping sharply at the onset of the Covid pandemic before increasing to a peak of 268 deals in Q1 2022. The level of European M&A activity in the US has now actually fallen below pre-pandemic levels of dealmaking (110 deals in Q3 2023).

The significant – and clearly unsustainable – growth in transatlantic deal volumes through 2021 and into 2022 has normalised during the extraordinary economic environment we have encountered in 2023. The apparent loss of confidence of European buyers in transatlantic dealmaking is of some concern – with the number of European acquisitions in the US in Q3 almost half the level of the corresponding period in 2022. We will monitor Q4 data for signs of an improvement in European buyer appetite for transatlantic M&A.

Overview of transatlantic deal activity: Q3 2023

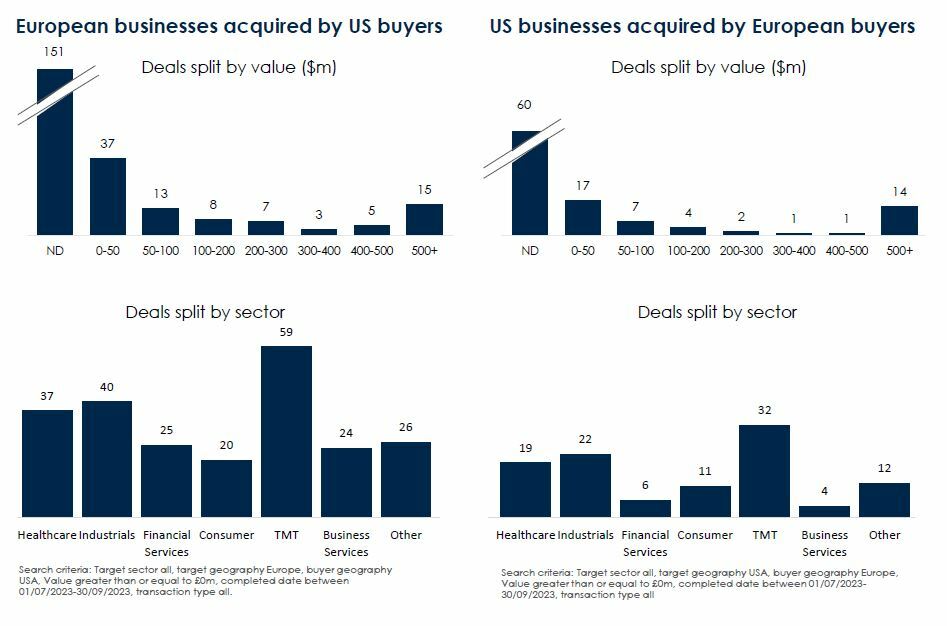

In terms of regional activity, the UK was the most popular country for US buyers during the quarter (37% of total deal volume), followed by Germany (17%), France (10%), the Netherlands and Italy (5% each).

Conversely, the UK was the most active European country in the quarter for acquisitions in the US (43% of total deal volume), followed by France (12%), Switzerland (10%), Germany and Italy (7% each).

European buyers in the US are predominantly making add-on acquisitions for existing operations (78% of total deal volume in the quarter). While US buyers in Europe are also making add-on acquisitions (58% of US deal flow in Europe in the quarter), they are bolder in terms of new platform acquisitions (42% versus 22%).

Continued Strong Transatlantic Aerospace & Defense Activity

Interest in the acquisition of Aerospace & Defense assets remains robust, with near-record deal volumes in recent years, given the financial resilience and projected near-term growth of the sector. Drivers of strong transatlantic M&A activity in the sector include:

Acquiring Mission Critical Technologies

- Filling portfolio gaps and expanding into attractive adjacencies

- Acquiring key talent and/or certifications

Strengthening International Positioning

- Leveraging strong US or European market presence with complementary international

positions, becoming “local” on the other side of the Atlantic

- Gaining new markets for existing products and capabilities

Gaining Customer and Program Access

- Acquiring companies with strong and trusted customer relationships

- Gaining access to established or near-term programs for which it would be difficult to compete without a local presence

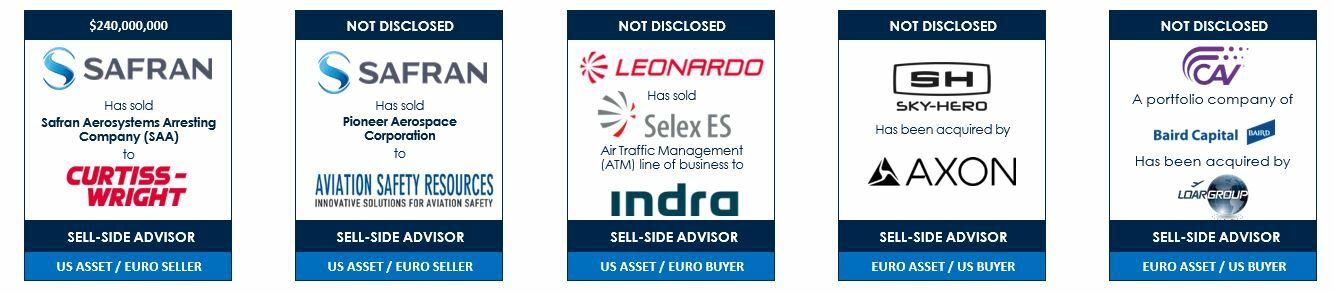

Select Stephens recent transatlantic Aerospace & Defense transactions

About the Experts