Market Trends

Stephens will never ask clients or prospective clients for personal or financial information, or provide investment advice, via social media, or WhatsApp.

If you have any questions or concerns about someone from Stephens contacting you, please call your Stephens Representative or reach out to us via our Contact Us form.

We provide investment banking, research, sales and trading, asset and wealth management, public finance, insurance, private capital, and family office services.

We are a family-owned financial services firm that values client relationships, long-term stability, and supporting the communities where we live and work.

The idea of family defines our culture, because each of us knows that our reputation is on the line as if our own name was on the door.

Our reputation as a leading independent financial services firm is built on the stability of our longstanding and highly experienced senior executives.

We are committed to bettering the communities where we live and operate. We do this by supporting corporate philanthropy, economic and financial literacy advocacy, and professional success.

Stephens is proud to sponsor the PGA TOUR, LPGA Tour, and PGA TOUR Champions careers, as well as applaud the philanthropic endeavors, of our Brand Ambassadors.

Stephens is the official investment banking partner of Williams Racing, one of the most winning teams in F1 history. We share that tradition of success.

We host many highly informative meetings each year with clients, industry decision makers, and thought leaders across the U.S. and in Europe.

Market Trends

Renewable energy, such as wind and solar, is a main discussion point in the energy sector that generates excitement about the possibility of cleaner and more sustainable energy sources to power our world. While the goal of achieving a complete energy transition by 2050 initially showed promise, a slowing consumer demand for renewable energy and reliance on governmental policy/tax credits for implementation has drastically changed the timeline. In early 2023, global insurance carriers began to implement practices to support this goal, which included reducing their books of business to net-zero carbon emissions by 2050. However, even those markets have backtracked their lofty implementation goals for a number of reasons.

Global demand for energy relies heavily on oil and gas, and the U.S. is no exception. The continued rise of renewable energy costs has resulted in countries reinvesting in coal-powered energy to support local consumers who have already seen other commodity costs rise due to inflation. This demonstrates not an energy transition, but an energy addition, as energy consumption grows worldwide.

When the phrase “energy transition” gained traction in 2019, and large government tax credits became available to incentivize the effort, many investors eagerly sought out new projects in the renewable energy sector. They anticipated investing in a new type of infrastructure that would produce revenue for years, as demand for renewables would continue to rise. Yet this has turned out to be not a consumer demand-driven market, but a policy-implemented market, meaning a complete transition to achieve net zero will occur much farther in the future than anticipated – if it ever occurs at all.

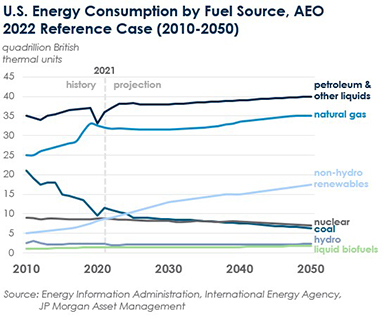

Current consumer trends show a heavy reliance on petroleum, natural gas, and coal, which make up 79% of all U.S. energy consumption. Comparatively, renewable energy only makes up 13% of U.S. energy consumption. With oil and gas production soaring to new heights amid strong global demand, a feasible path to eliminating oil- and gas-based energy is far from clear. For example, this year China is poised to overtake the U.S. as the world’s top oil consumer.

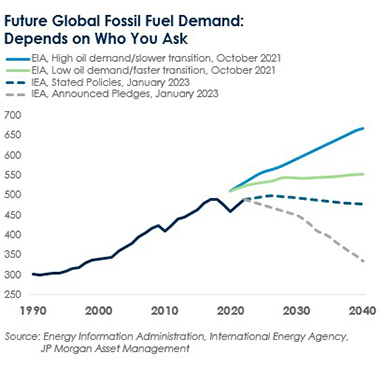

This chart demonstrates International Energy Agency (IEA) projections for lower fossil demand, based on the current stated policies and “announced pledges” that have not gained traction to keep up with the 2050 net zero timeline. Conversely, the Energy Information Administration (EIA) predicts oil demand to rise in both “transition” scenarios.

The projected 2050 total energy use still frames petroleum and natural gas as the main supporter of energy consumption in the U.S., with renewable sources growing steadily over the next couple of decades. In fact, petroleum, liquid fuels, and natural gas consumption is expected to rise by 2050 and will continue to be a leading energy resource in the U.S.

Despite renewable energy’s growth rate over the last few years, snapshots of growth do not capture the whole picture for the energy sector. Equating these renewable energy data snapshots to overall energy consumption could lead to unsubstantiated conclusions. An analogous conclusion would be to assert that that because Fort Meyers, FL, is the fastest growing city in the U.S., it will become larger than Los Angeles, Houston, and New York City, provided further tax credits and government intervention make that happen. Obviously, this is a very unlikely scenario. Likewise, some participants in the energy industry utilize snapshots of growth to portray data that supports 2050 as an attainable net-zero goal. The broader view of data indicates otherwise.

How can the replacement of oil and gas be possible if the energy transition is already behind schedule? According to many energy transition experts, the solution is to implement more tax credits and additional federal restrictions on oil and gas, while persuading the public to trust that adoption of renewable energy is on track and that the electric grid will support their needs.

Early energy transition adopters contributed to this idea by abandoning their combustion engines to invest in electric vehicles. At the time, this seemed to be a cheaper option, but this view failed to take into account the human capital cost and the reliance on the electric grid for everyday transportation.

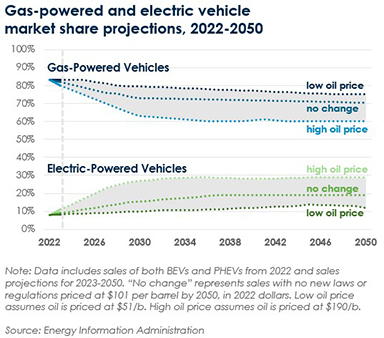

According to the EIA, projections for 2050 show electric vehicles will account for fewer than one-third of all vehicles in the U.S., unless additional tax credits are provided or the government imposes further policy restrictions on gas-powered vehicles.

If oil prices remain stagnant, the projected decrease of gas-powered vehicles by 2050 is only 10%. In the scenario of steady gas prices, the number of electric vehicles is only projected to rise from 5.8% to 12% of the total vehicles in the U.S. by 2050. While insurers had their eyes set on reducing their books of business to net zero by 2050, consumers are not making the switch to electric vehicles as quickly as originally thought.

Skepticism abounds in the U.S. about investing in a new form of transportation without guarantees of an uninterrupted electric grid to support the current needs of the population, especially if EV adoption requires further governmental policies.

California, a leader on this front, implemented a ban on new gasoline / petrol vehicles by 2035 in hopes of creating the infrastructure to support clean energy usage. A 2023 article published by Cal Matters explored the situation in California and the likelihood of meeting these goals. “Despite expecting 12.5 million electric cars by 2035, California officials insist that the grid can provide enough electricity. But that’s based on multiple assumptions — including building solar and wind at almost five times the pace of the past decade — that may not be realistic.

Cal Matters quoted David Victor, a professor and co-director of the Deep Decarbonization Initiative at UC San Diego. He said that, in order to produce enough energy, “We’re going to have to expand the grid at a radically much faster rate. This is plausible if the right policies are in place, but it’s not guaranteed. It’s best-case.” To make this happen, further governmental policy implementation will be needed, even if consumer demand does not yet rise to meet production.

California could face significant costs if these goals go unmet and rampant production of renewable energy facilities fails to meet the needs of its citizens. California produces less than 3.3% of the total energy in the U.S. and is not a top 10 state for U.S. energy production. The top 10 producing states are: Texas (24.2%), Pennsylvania (9.9%), Wyoming (6.1%), West Virginia (5.2%), New Mexico (4.9%), North Dakota (4.5%), Oklahoma (4.7%), Louisiana (4%), Colorado (3.9 %) and Ohio (3.3%). These states generate nearly 71% of the energy in the U.S., with the majority coming from oil, gas, and coal.

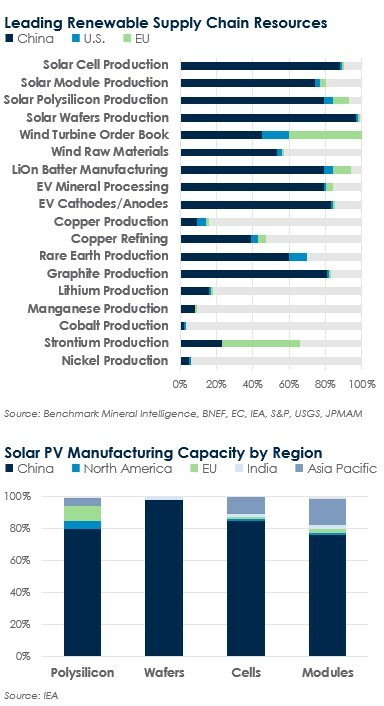

Regions in the U.S. shifting to renewable energy production also rely on other countries for parts and resources. China has the majority of the market share for renewable energy materials, and the U.S. depends on China for 80% of the rare earth metals needed for renewable energy infrastructure. Insufficient domestic parts and materials production can present supply chain vulnerabilities and other strategic gaps. Unless the U.S. becomes self-sufficient regarding production and materials, a complete energy transition will be even less likely to occur in the next few decades.

Blanket policy implementation across the globe does not factor in what life is like in certain oil- and gas-based regions. For instance, Midland, TX, and San Francisco, CA, do not have many commonalities. But global insurers view both regions as needing to abide by the same ESG regulations in order to receive proper insurance coverage.

Though less prevalent than renewable energy (wind and solar), carbon capture utilization storage (CCUS) systems have been central to oil, gas, and industrial firms’ discussions regarding a path to reducing carbon emissions. Although critics claim that CCUS is ineffective and too costly to scale on a global basis, many energy firms have retrofit facilities to adapt these sequestering systems in efforts to become more sustainable. With further development, this technology can be implemented to curb emissions at the source of production without having to build a completely new infrastructure that relies on weather trends. In addition, captured carbon can be stored and utilized to produce sustainable fuel as well as cleaner oil and gas byproducts such as clothing, chemicals, plastics, and more. As a result, CCUS has the potential to reduce costs for consumers around the world. It also presents an alternative to attempting to remove oil and gas completely, which might significantly raise costs for these products along with prices for groceries and household materials.

Since there is no evidence that a complete “energy transition” will occur in the near future, it is more accurate to describe renewable energy as an “energy addition” to our current infrastructure. Furthermore, moving away from oil and gas quickly, without careful analysis of the broader macroeconomic factors, may have unintended consequences for energy output across the country. Instead, sufficient investments in domestic E&P, Midstream, and Downstream firms can help to both avoid such outcomes and to improve sustainability by reducing excessive byproducts production.

When underwriting accounts, insurers often scrutinize clients for risk quality, growth opportunity, and potential long-term revenue. Based on prevailing trends, it is possible that underwriters for the oil and gas sector may eventually decide not to provide an insurance quote due to global policy implementation rather than risk quality and opportunity for financial growth. Risk managers in the oil and gas sector need to understand the market’s long-term goals for their book of business and start making decisions early in order to prepare their insurance programs for the future.

Starting a captive program can be one of the best ways to prepare for the insurance market of tomorrow. With enough funding in a captive or a captive cell, insureds will be able to leverage capacity and pricing in the market, which will be vital to counteract any changes in capacity. Firms that invest in their risk management and insurance program today can help alleviate future insurance budgets and create a more flexible program.

At Stephens, we understand how an array of fast-evolving factors in the energy sector are impacting the insurance considerations of those firms. Some brokers have internal branches of their firm pushing the energy transition, while still communicating support to their oil and gas partners. Mixed messages on sustainability can lead to confusion among clients about their brokerage partner’s goals and support services. Stephens fully supports our oil and gas clients, and we understand that renewables have significant progress to make as an addition to the energy space before any meaningful transition occurs.

Click here for a printable version of this article.