December CPI Rose 0.3 From the Previous Report

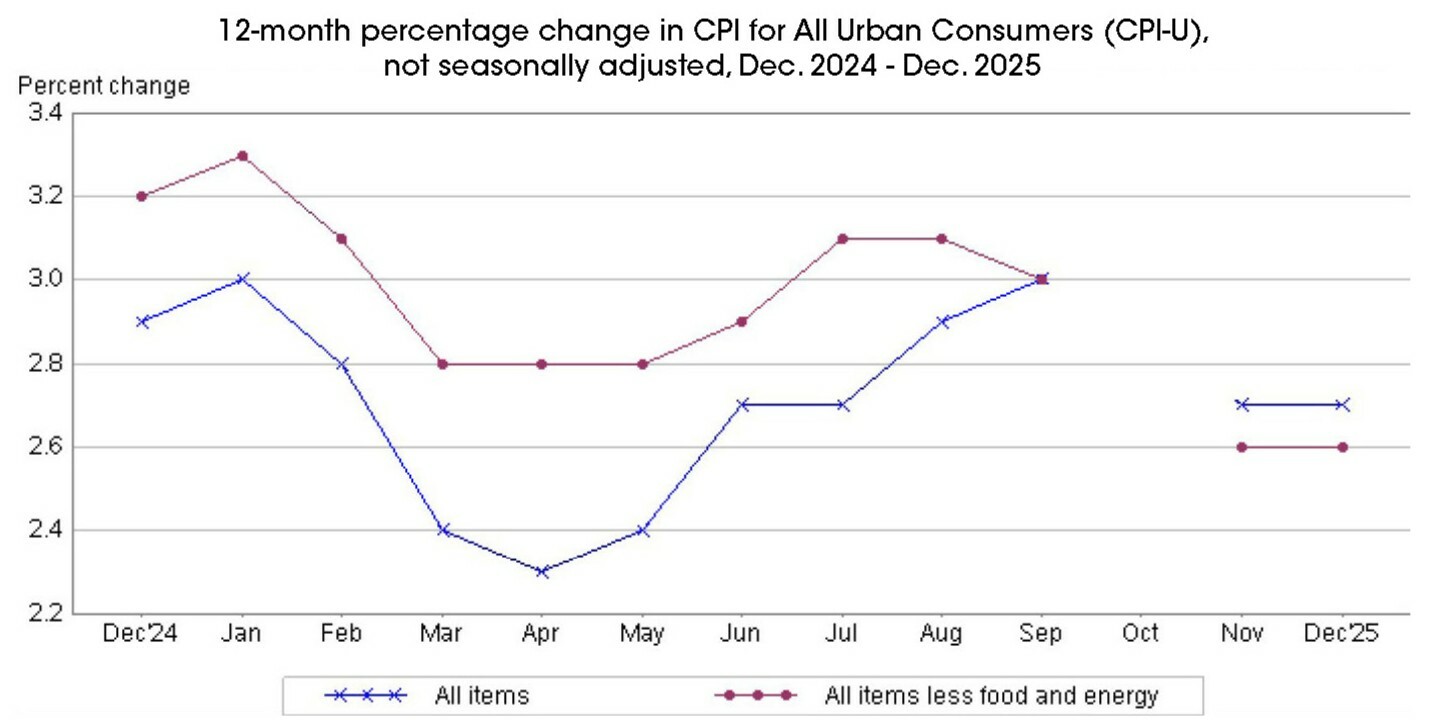

The December Consumer Price Index (CPI), a key gauge of inflation that measures changes in prices paid by consumers across a broad basket of goods and services, increased 0.3% from November and rose 2.7% year-over-year. This result was consistent with November’s year-over-year reading, suggesting that inflationary pressures remain persistent but have stabilized in recent months rather than reaccelerating.

Shelter costs, historically the most persistent and influential component of CPI, rose 0.4% month-over-month in December and continued to be the primary driver of headline inflation. Elevated housing-related costs have remained a challenge for overall disinflation, reflecting ongoing tightness in rental markets and the lagged effects of higher mortgage rates.Energy prices increased 0.3% month-over-month, marking a moderation from November’s 1.1% gain. Notably, gasoline prices declined 0.5% during the month, helping offset increases in other energy components. The continued easing in gasoline prices is a positive development for consumers, as lower fuel costs tend to provide immediate relief to household budgets and can support consumer spending by putting more discretionary income back in consumers’ pockets.

Overall, the December CPI report reinforces the narrative that inflation is no longer rapidly cooling but remains on a steady, elevated path. While progress toward the Federal Reserve’s 2% inflation target has been made, stubborn shelter costs and uneven progress across categories suggest the final leg of disinflation may take longer than initially expected.

CPI Home: U.S. Bureau of Labor Statistics (bls.gov)

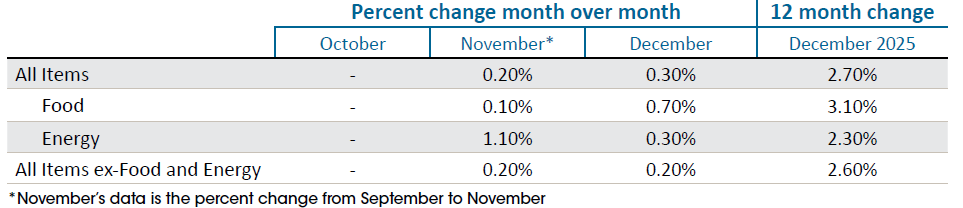

The table below shows m/m percentage changes in CPI indexes which include Core CPI, Food and Energy (Core CPI excludes Food and Energy).

Source: Consumer Price Index Summary (bls.gov)

Fed Focus: Inflation Still Above Target

One of the Federal Open Market Committee’s (FOMC) two primary mandates is price stability, with inflation targeted at a long-term rate of 2%. Despite meaningful progress over the past year, inflation remains above this objective, reinforcing the Committee’s cautious policy stance. The FOMC has consistently communicated its willingness to use all available policy tools to ensure inflation returns sustainably to target, underscoring its commitment to maintaining restrictive financial conditions until sufficient progress is achieved.

Next Fed Decision

Looking ahead, the upcoming January FOMC meeting, scheduled for January 27–28, 2026, is widely expected to be a non-event from a policy standpoint. Market-implied probabilities suggest only a 5% chance of a 25 basis point rate cut at this meeting, reflecting expectations that the Fed will remain on hold as it assesses the cumulative impact of prior tightening and incoming inflation data. As a result, investors are likely to focus less on immediate policy action and more on the tone of the Committee’s statement and Chair Powell’s commentary for clues regarding the timing and pace of potential rate adjustments later in the year.

- The information in this CPI Update has been prepared solely for informative purposes and is not a solicitation, or an offer, to buy, sell or hold any security or a recommendation of the services supplied by any money management organization. It does not purport to be a complete description of the securities, markets or developments referred to in the report. We believe the sources to be reliable, however, the accuracy and completeness of the information is not guaranteed. We, or our officers and directors, may from time to time have a long or short position in the securities mentioned and may sell or buy such securities. Data displayed on this site or printed in such reports may be provided by third party providers. The indexes referenced in the charts presented are unmanaged and do not reflect any transaction costs or management fees. They were chosen to give you a basis of comparison for market segment performance. Actual investment alternatives may invest in some instruments not eligible for inclusion in such an index or model and may be prohibited from investing in some instruments included in such an index or model. This document is intended only for the addressee and may not be reproduced or redistributed. If the reader is not the intended recipient, you are notified that any disclosure, distribution or copying is prohibited. Additional information is available upon request. Please contact your Financial Consultant with any questions.