Market Trends

Stephens will never ask clients or prospective clients for personal or financial information, or provide investment advice, via social media, or WhatsApp.

If you have any questions or concerns about someone from Stephens contacting you, please call your Stephens Representative or reach out to us via our Contact Us form.

We provide investment banking, research, sales and trading, asset and wealth management, public finance, insurance, private capital, and family office services.

We are a family-owned financial services firm that values client relationships, long-term stability, and supporting the communities where we live and work.

The idea of family defines our culture, because each of us knows that our reputation is on the line as if our own name was on the door.

Our reputation as a leading independent financial services firm is built on the stability of our longstanding and highly experienced senior executives.

We are committed to bettering the communities where we live and operate. We do this by supporting corporate philanthropy, economic and financial literacy advocacy, and professional success.

Stephens is proud to sponsor the PGA TOUR, LPGA Tour, and PGA TOUR Champions careers, as well as applaud the philanthropic endeavors, of our Brand Ambassadors.

Stephens is the official investment banking partner of Williams Racing, one of the most winning teams in F1 history. We share that tradition of success.

We host many highly informative meetings each year with clients, industry decision makers, and thought leaders across the U.S. and in Europe.

Market Trends

On the heels of recent T&L sector volatility, corporations are sharpening focus on their core lines of business. Going forward, we believe corporate divestiture activity (or “carve-outs” as referred to in this analysis) may become an increasingly important strategic lever for value creation.

When considering a divestiture, a number of factors should be evaluated, as detailed below, including the recognition that separation value extends beyond the headline purchase price. Disciplined planning can reduce separation cost and effort, while potentially improving transaction certainty and maximizing net proceeds.

When a Company Should Consider a Divestiture

When undertaking a strategic review to ascertain whether a division is a divestiture candidate, the following high-level questions are a helpful test for boards and

management teams to evaluate whether continued ownership and investment into a business line makes sense:

Once a Parent company deems a business non-core, taking action to develop a divestiture plan is critical. In our experience, business segments deemed non-core are typically under-resourced, suffer from elevated turnover and low morale, become less competitive, and, therefore, value erodes over time. Proactive divestitures can strengthen strategic focus, improve capital allocation and returns, and support a clearer ownership narrative.

Sell-side Guide – Investing in Preparation is Critical to Unlocking Value

Divestitures are more complex and time-consuming than regular-way M&A. Rigorous preparation is paramount to create a market-ready opportunity with a clear transaction perimeter, clean financials, and an executable separation plan.

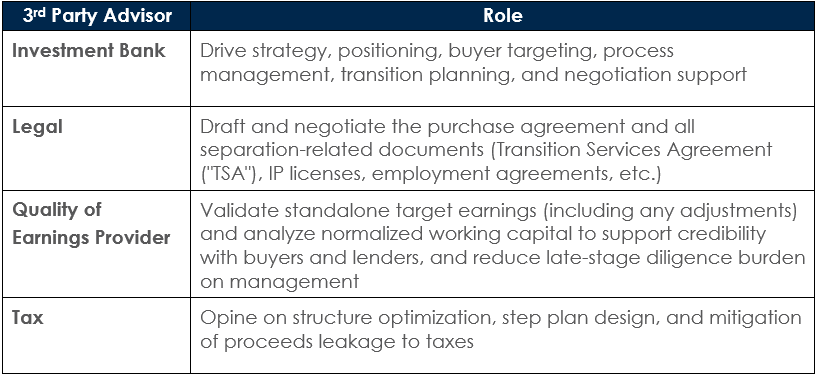

As a best practice, the Parent company should assemble a team of 3rd party advisors with carve-out experience to support value optimization, efficient execution, and certainty of a transaction, while reducing ongoing support burdens and operating limitations of the Parent. A typical 3rd party advisory team to support a carve-out transaction would include the groups below, each with their own area of focus:

Step 1: Defining a Transaction Perimeter and Establishing a Separation Plan

At the onset of considering a divestiture, the initial focus needs to be on establishing a transaction perimeter, which involves identifying the key components of the business that will transfer to a new owner. In parallel, the Parent should begin building an executable separation plan that defines how the business will operate on Day 1 and how remaining dependencies on the Parent will be unwound post-closing. Developed together, these two workstreams could reduce buyer uncertainty, support credible carve-out financials, and possibly minimize late-stage surprises that can drive delays or re-trades.

Standard transaction perimeter items to consider include:

Separation plan components that the Parent should focus on include:

Step 2: Preparing Clean Financials

Once a perimeter and a separation plan have been established, the Parent's focus should shift to preparing pro forma financial statements for in-scope operations. The financials should reflect the revenues and costs associated with all perimeter-defining items, as well as requisite standalone costs. For a portion of the financial statement line items, this is often as straightforward as revised general ledger and trial balance mapping; however, for other line items, such as corporate overhead, contemplating allocation methodologies in detail is necessary to produce marketing-ready, clean financials. Sellers should also give early attention to pro forma personnel costs, including any headcount additions required to replace shared services, and benefits normalization where the divested business has historically participated in Parent-level plans. These adjustments are often assumption-based and, as a result, can drive re-trades or disagreements on standalone earnings if poorly considered. Ultimately, buyers will expect corporate support expenses to reflect true cash costs as opposed to some other internal accounting methodology (i.e., percentage of revenue). Corporate cost allocations often take considerable time and thought to keep assumption-based expenses logical and defensible during buyer diligence.

Step 3: Drafting the TSA Services Schedule

The TSA is a contract under which the Parent provides specified transitional services to the divested business beginning Day 1 and continuing for a defined period. The TSA typically sets the scope of services, service standards, pricing, governance, and an exit timeline as the divested business stands up standalone capabilities. Although the TSA agreement and its details will be primarily drafted and negotiated during the process, planning ahead for the services a buyer may require is critical to effectuating a seamless transition of ownership from the Parent. For this exercise, Parent should develop a preliminary list of services currently provided by the Parent to the divested entity that will still be required post-close, together with descriptions of those services, the required personnel, the cost to deliver, and an estimated separation timeline. In our experience, being prepared with a well-formed TSA services schedule often minimizes timing delays and value leakage associated with an expanded scope of services post-close.

Key Stumbling Blocks to Avoid: Common issues that could derail carve-out transactions or cause value leakage:

Parent Non-compete: Non-compete language in the purchase agreement is standard protection for a buyer. Appropriately tailoring such language to avoid go-forward impediments to the Parent is critical for post-transaction continuity.

Stephens’ Carve-out & Divestiture Experience: Over the course of the last ~15 years, Stephens’ T&L group has built one of the leading carve-out and divestiture advisory practices.

For more information on Stephens’ divestiture and carve-out capabilities, please contact any of the authors below: